|

| Mark Strozier Chance |

How does the bank decide to lend you money?

When you talk about lending, you have to talk about Credit Scores. These are often referred to as FICO scores.

*Disclosure: My best advice would be to listen to Dave Ramsey and stay debt free for the rest of your life. But if you still believe in credit, and you want to build a great credit score... this page will provide some things you need to know.

What is a FICO score?

Many people want to know what a FICO score is. FICO stands for the Fair Isaac Corporation, founded in 1956 and in 2009 renamed: FICO. This is the one company that has more control over your interest rates and loan approvals than any other. They review your credit reports and create a score based on the information found there.

The formula that determines that score is TOP SECRET. The banks don't even know it. We do know a few things about the score though.

The Credit Scores can vary from 300 to 850; recently information has come out that it may go into the 900's now. A “Good Score” is hard to determine because different lenders have different cut off marks. According to Wikipedia the average marker in the USA is about 640.[1] This score is about the breaking point between bad and good.

Typically, though, banks are looking for scores in the 700’s.

~www.MyFico.Com~

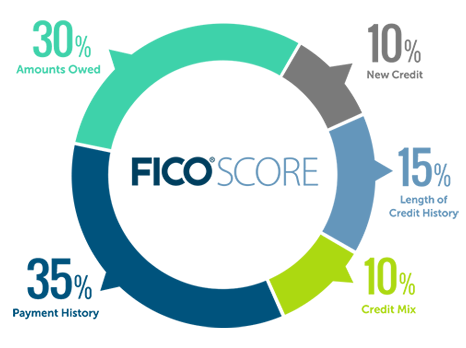

The following are the categories that FICO uses and the percentages showing the importance of each category. This information was taken directly from www.myfico.com:

Payment history 35% (Were you late or on time?),

Amounts Owed 30%,

Length of credit history 15%,

New credit 10%,

Types of credit used 10%.

If you pay all of your bills on time and you are never late you have overcome half of the battle with FICO. Another thing to keep in mind is history. It is recommended that you keep between one to three credit cards and no more. Keep one for as long as possible. This history factor doesn't so much take into account the old closed accounts you have in your history as much as it wants to see the oldest account you have that is still currently open. If you are closing out credit card accounts keep the one that has been open the longest.

~Pay On Time~

Pay your bills on time. If it has already been charged off to collections realize that paying off collections will not remove it from your credit report, it will stay there for seven years. The seven year period starts at the last date of contact or payment[2]. If it has been 6 years and you call them about anything your seven years could start over.

Additionally the creditor could sell your debt to another collector and that could restart their clock too. There is much more too it than this so seek a reputable credit counselor if you have trouble making payments. If you believe it has been more than 7 years since you last dealt with the debt you should dispute it with the credit reporting agency under the Fair Credit Reporting Act (FCRA) and a clause known as Date of Last Contact/Activity (DOLA). Of course you should pay if you are able.

~Low Balances~

Keep balances low on credit cards and all open revolving credit. Never use more than 45% of the available credit. This means that if you have a credit card that has a spending limit of $5,000 you never want to use more than $2,250 of that limit. Simply take your limit and multiply that by 0.45 to find out how much you can actually use. If you go over from time to time it's OK, but not if you are trying to take out a large loan soon and not on a regular basis.

You should be paying it off in full every month anyway, even if you are using no more than 45% of your limit. Do not close cards just to raise your credit score and do not move money around from card to card. Just pay it off. Closing cards because you have too many, however, can be a good thing long term. Again seek an experienced reputable credit counselor on this.

The only time moving money around in balance transfers is good is if that helps you consolidate your bills into one place with a lower interest. This may not help your score short term; but it will help you pay it all off faster which affects your score long term. Keep no more than 3 credit cards at any given time open. If you want to close your card once it has been paid off make sure to call and close the card. Don't assume that it will close just because you paid it to a zero balance. It looks better if you close the card than if the credit card company closes it due to inactivity.

~New Credit~

New accounts can lower your credit score and a rapid build up of credit accounts is a big red flag! Open one to two credit cards over time and no more, keep them and use them wisely as stated above.

Research, Research, Research.

Make sure you are in the right loan or card for you. Pull your own credit first before looking, this doesn't count against your score. Use credit responsibly, here are a few tips. Apply for new credit accounts only as needed. Use it correctly. Closing an account does not make it go away. It stays on the report 7 years.

Paying off collections doesn't make the account fall off of your credit report or improve your score all that much if any; but may have legal and or long term benefits. The Word of God says to owe no man anything but love. Therefore you should always seek to pay your’ debts. It also laid the foundation of our bankruptcy laws clearing debts and offering a start over. Allow the Spirit to lead you in your decisions regarding past debt.

Fixed payment and fixed term loans are often better than open revolving credit. Have five or less open credit accounts on your file and make sure that only two of them are revolving accounts like credit cards or lines of credit. Pay loans on time and pay credit cards off in full each month. Use no more than 45% of your credit cards/LOC available limits.

~DSR or DTI~

The better your score the better the interest rate and the higher the chance your loan is approved. The score isn't the only factor in approving loans. Many people with HIGH credit scores are turned down due to a high debt to income ration, known as DTI. This is also known as Debt Service Ration or DSR.

~Deeper Look at DSR or DTI~

Here is a quick look at DTI/DSR and the loan approval systems that are out there. The concept of DTI (Debt To Income), also known as DSR (Debt Service Ratio), is summarized as the amount of debt the person has compared to the amount of income they bring in and how they use it all. A person has a better chance of getting approved for credit products when they don’t need them because they have the income to support the debt.

If the person looses their job they often want to apply for credit to help out during the time it takes to find a new job. By that time it's too late because their DTI is higher without income or on unemployment income. If you feel that you would in the future desire to have a line of credit for emergencies, apply ahead of time before you would actually need it. Its irony, those who don't need it usually qualify over those who do.

Debt to income is a formula. Debt divided by income. An Example helps here.

~Example of DSR or DTI~

The first section for open credit reflects available limits and for closed credit reflects the original loan amount. The balance is the current balance on the account. This will be the balance at the time the credit was last reported. It doesn't matter if you pay your balance in full every month, this will be used to calculate your DTI this is one of the reasons you want to keep your card balances under 45% of the limit.

The payment section will show the payments you've been making. If there is no payment: such as a credit card you haven't used or a student loan that's being differed the creditor may calculate a payment that could be due. This is in order to figure out if you could afford the new credit AND the existing credit.

Let's say that the person in the example above makes $45,000 a year. The lender will take that and divide it by 12. This gives the borrower $3,750 per month. Lender usually uses GROSS income, before taxes, because it's really not their business what two people making the same amount choose to deduct for health insurance or other deductions.

This person has a debt payment of $2150. So $2150/$3750 = 57.3% This person has a Debt To Income (DTI/DSR) of 57.3%. Most lenders require less than 45-50%. Markets change and lenders vary on this, but this is the concept they are addressing.

~Usage~

They may also take a look at your usage. This comes from taking your available credit on open lines and figuring out how much you use. This is where keeping your credit card balances low even if you pay them in full every month comes into play. Line usage refers to the amount of your open line limits that you use. In this persons case they have $9,500 in credit card balances and $12,000 total available limits. $9,500/$12,000=79.2%

That is 79.2% line usage. Lenders usually like to see less than 45% Line usage.

The BEST way to use a credit card (from a FICO score building perspective) would be to keep the card paid in full, go out once a month and buy ONE small item (Dr. Pepper, Coffee, Monster) from the Walmart self-check out or starbucks. Something you would have bought with your cash anyway.

WAIT for the statement, and then PAY IT IN FULL.

Rinse, Repeat. Do this every month for 24 months, and watch your FICO climb.

~Balances~

Another factor that they look at when lending is balance in use. Lenders like to see that only a certain percentage of a person’s annual salary is tied up in open line balances. The general rule is less than 25-30% of the annual salary should be tied up in line balances.

If the person above makes $45,000 per year that means 25% of their income is $11,250. They are using $9,500 of their open credit. Therefore this person is using 21% of their income on line balances, ($9,500/$45,000=0.211) which is less than 25% of their income on open revolving lines.

~Example Person’s Results~

To review, this person has: DTI/DSR: 57.3%, usage of: 79.2%, total balance in use of 21% of annual salary. Even if the persons FICO is good and they have been with their employer longer than 2 years, the lender may still see the DTI/DSR and usage as too high of a risk and may decline the loan.

This is how a person with a good FICO score and great income can still be declined on a loan/line request. I hope this helps you to understand the approval process better and begin to plan your finances to match up to this type of scrutiny. The lender is essentially asking one question: “Is this person a risk?”

If you aren't sure what your credit score or credit report looks like, you can always get them through the following resources and many other places:

Identity Theft Protection Services usually offer credit score tracking.

The “Big Three” credit bureaus are:

- Experian

- Equifax

- TransUnion

[2] http://consumerist.com/2007/04/negative-items-fall-off-credit-report-after-seven-year-itch-as-long-as-you-dont-scratch-em-creditors.html

The Insider

The Insider is a BIG fan of Dave Ramsey:

- Go read/listen/watch Dave Ramsey and he'll teach you how to do it right!

- Listen to The Dave Ramsey Show (HERE)

- Or by his most popular book: (HERE) The Total Money Makeover: Classic Edition: A Proven Plan for Financial Fitness

![[ { ENDER'S GAME } ] by Card, Orson Scott (AUTHOR) Oct-31-2006 [ Hardcover ]](https://i.gr-assets.com/images/S/compressed.photo.goodreads.com/books/1697162486l/199597832._SX98_.jpg)

0 comments:

Post a Comment

Be Nice, Be Kind, Be Thoughtful, Be Honest, Be Creative...GO!